November surge: Development ID doubles transaction volumes as 1-bed stock leads demand

11 December 2025

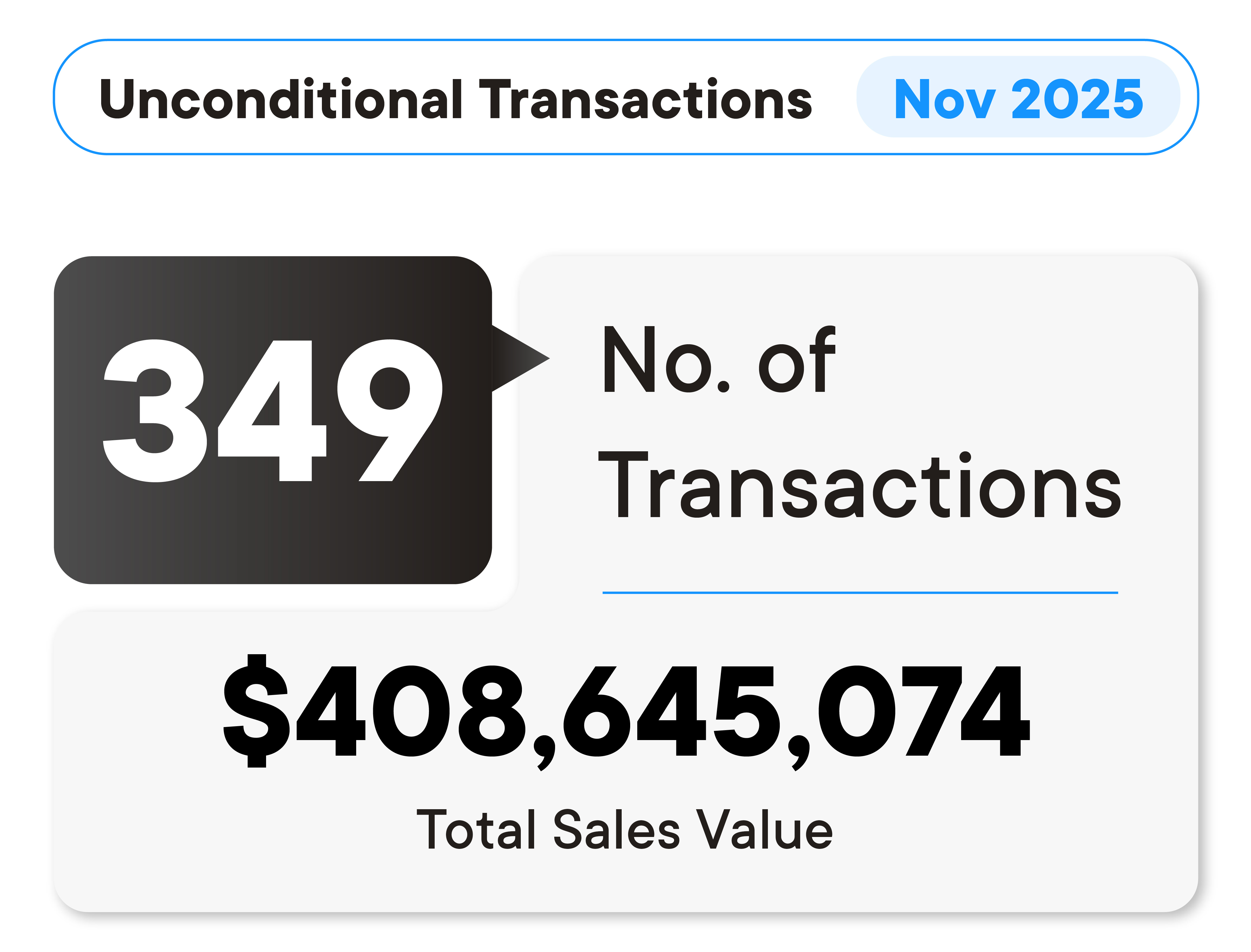

Development ID recorded a significant uplift in activity in November, with 349 unconditional transactions totalling $408.6M - almost double October’s sales volume and total value. The sharp rise reflects an increase in available stock across key projects and renewed confidence among investors seeking compact, well-located product.

November activity on Dev ID nearly doubled October

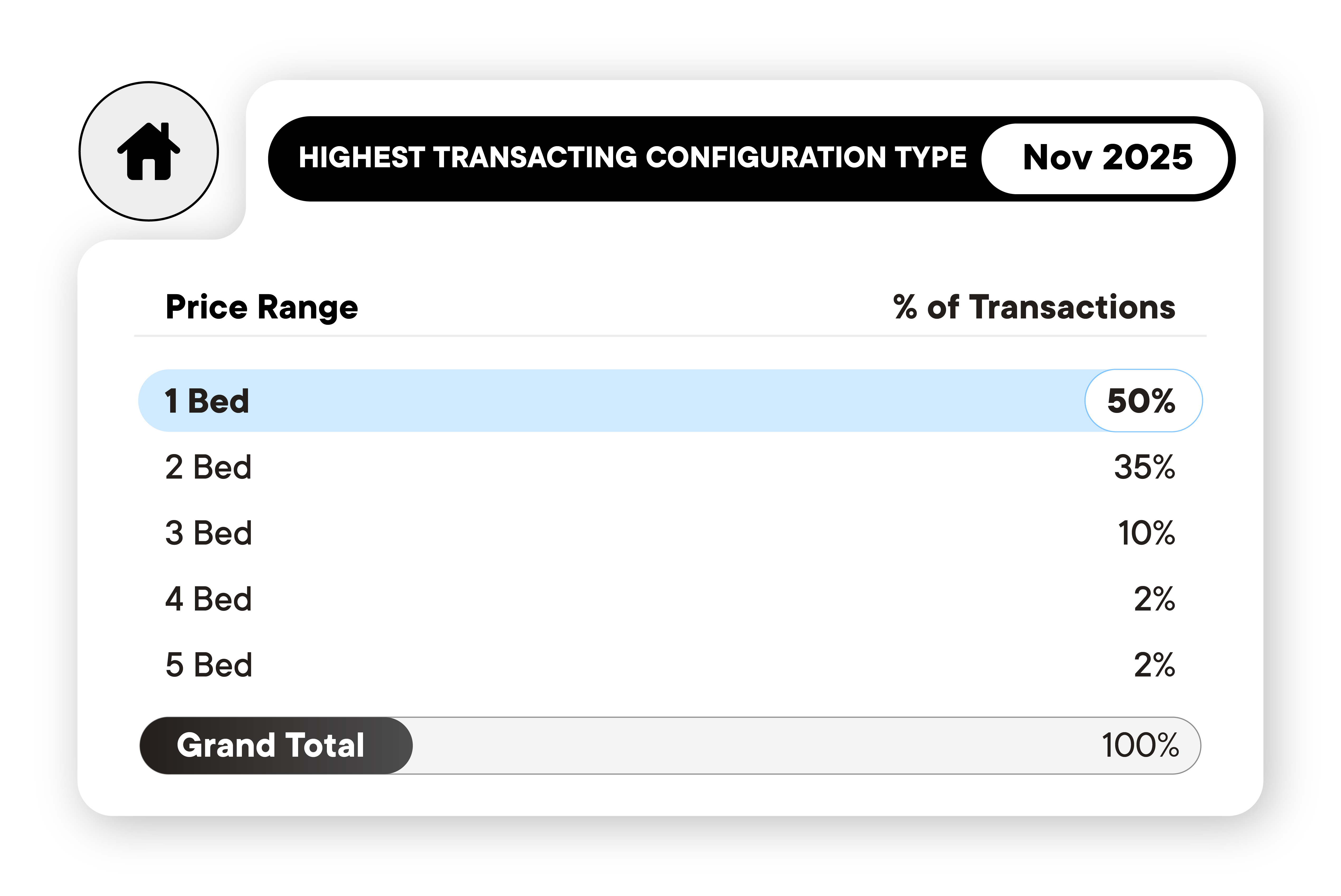

November transactions by bedroom configuration

November saw a clear shift back toward smaller configurations, reversing October’s tilt toward 3-bedroom stock.

1-bed stock transacted in November climbed to 50%

1-bedroom product surged, climbing from 30% in October to 50% in November - currently the highest-performing configuration by a wide margin.

2-bedroom stock remained strong at 35%, though still below September levels, suggesting solid but stabilising demand across the mid-tier.

3-bedroom dwellings accounted for 10%, down sharply from 35% in October.

4-bedroom and 5-bedroom configurations each represented 2%, maintaining the modest uplift first observed in October.

This return to compact stock dominance underscores investor appetite for rental-ready product and the growing appeal of smaller formats amid affordability pressures.

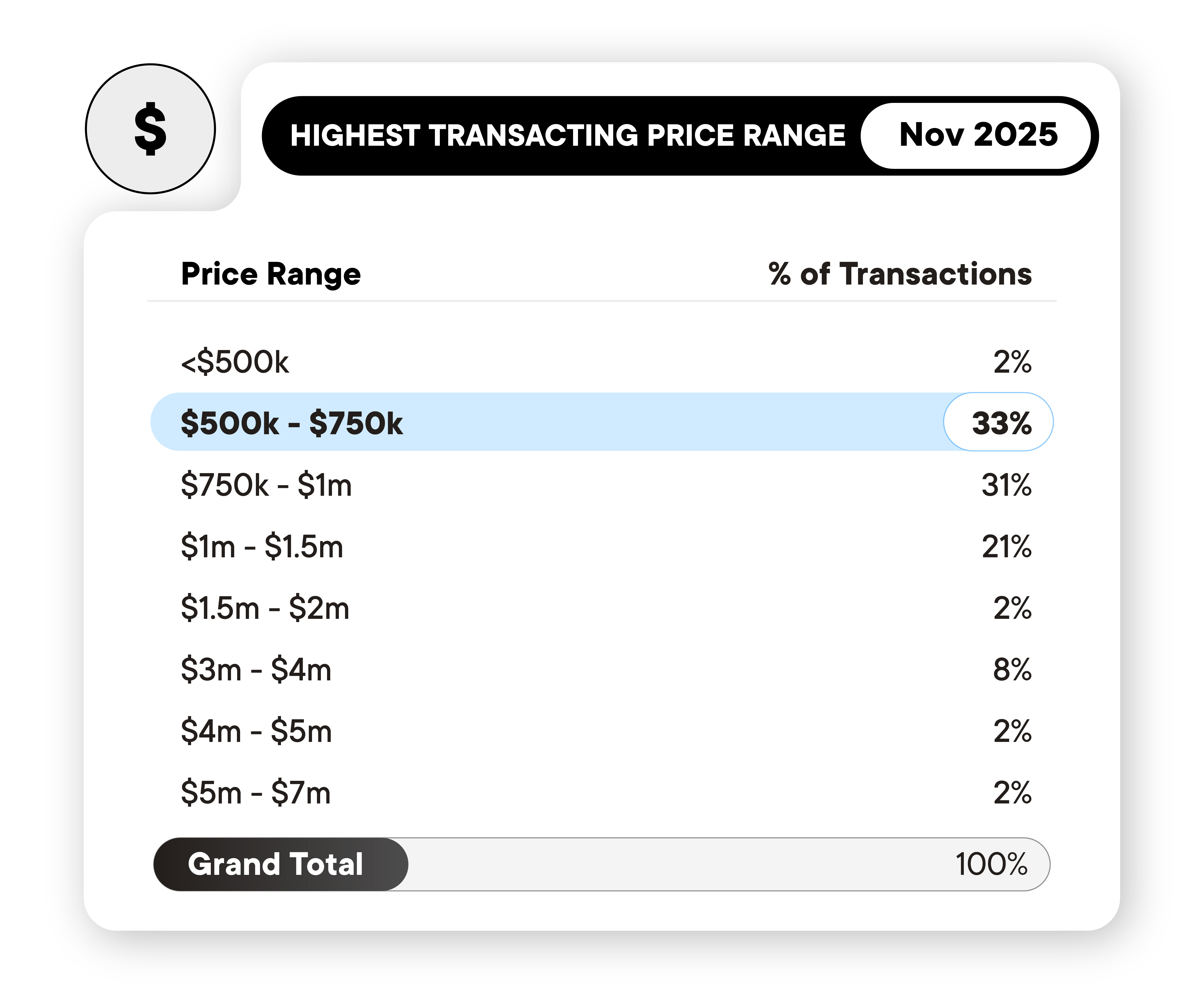

November transactions by price range

November delivered a more balanced spread across price segments, with activity strengthening meaningfully in the mid-market.

The $500k-$750k range led transactions in November at 33%

The $500k-$750k range led transactions at 33%, increasing from 18% in October.

The $750k-$1m bracket followed closely at 31%, slightly down from 22% in October but still a substantial share given the volume uplift.

The $1m-$1.5m range rebounded to 21%, recovering from October’s dip to 14%.

Entry-level product (<$500k) softened further to 2%, reflecting ongoing scarcity and limited national availability.

At the upper end, $3m-$4m product accounted for 8%, with smaller contributions from the $4m-$5m and $5m-$7m categories - highlighting continued, if selective, demand for prestige investment-grade stock.

Compared to October, the November price distribution shows renewed engagement across the $500k–$1.5m band - a segment typically aligned with investor and first-time buyer interest - while also retaining meaningful traction in the luxury bracket.

November’s results point to a lively end to the calendar year, with stronger stock volumes, heightened investor participation, and broad-based demand across both compact and mid-tier product.