We recently released our FY25 Q4 Off-the-Plan Market Insights Report which features valuable insights from Development ID, highlighting transaction trends from our extensive network of channel agent partners.

Below takes a further dive into national sales transacted through Development ID in FY25 Q4 compared to FY25 Q3.

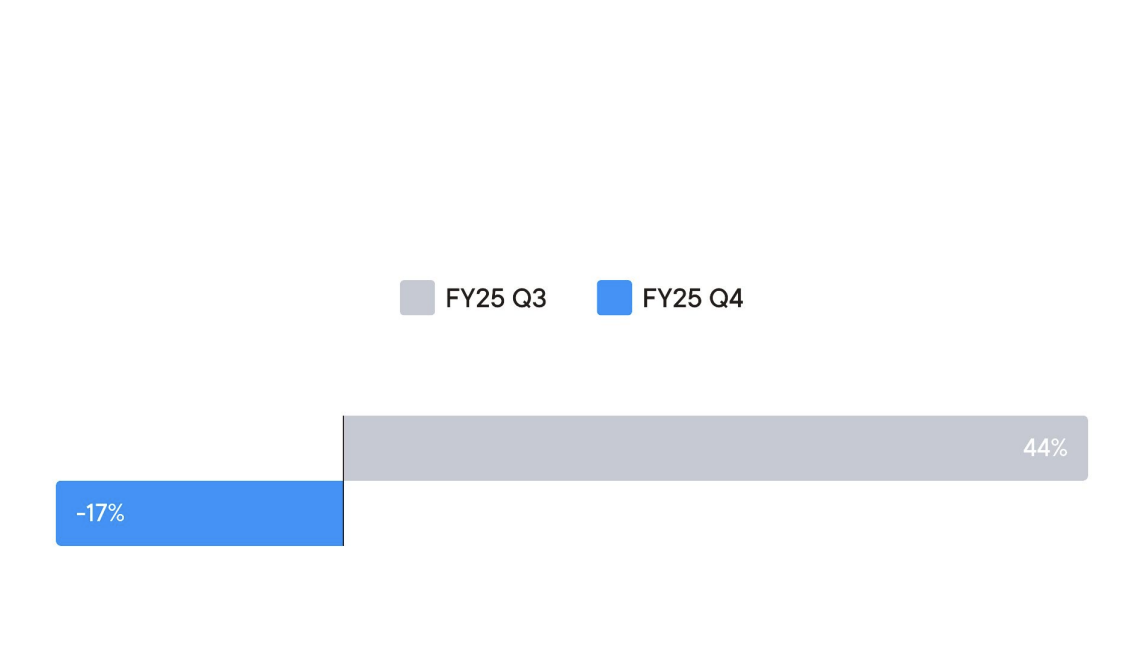

Sales Activity

Sales transacted through channel agent partners via Development ID declined nationally by 17% in FY25Q4, following a strong 44% uplift in FY25 Q3. The quarterly drop reflects a shift in available stock and transaction mix, with fewer compact, investment-grade dwellings available and a greater share of higher-value product influencing volumes.

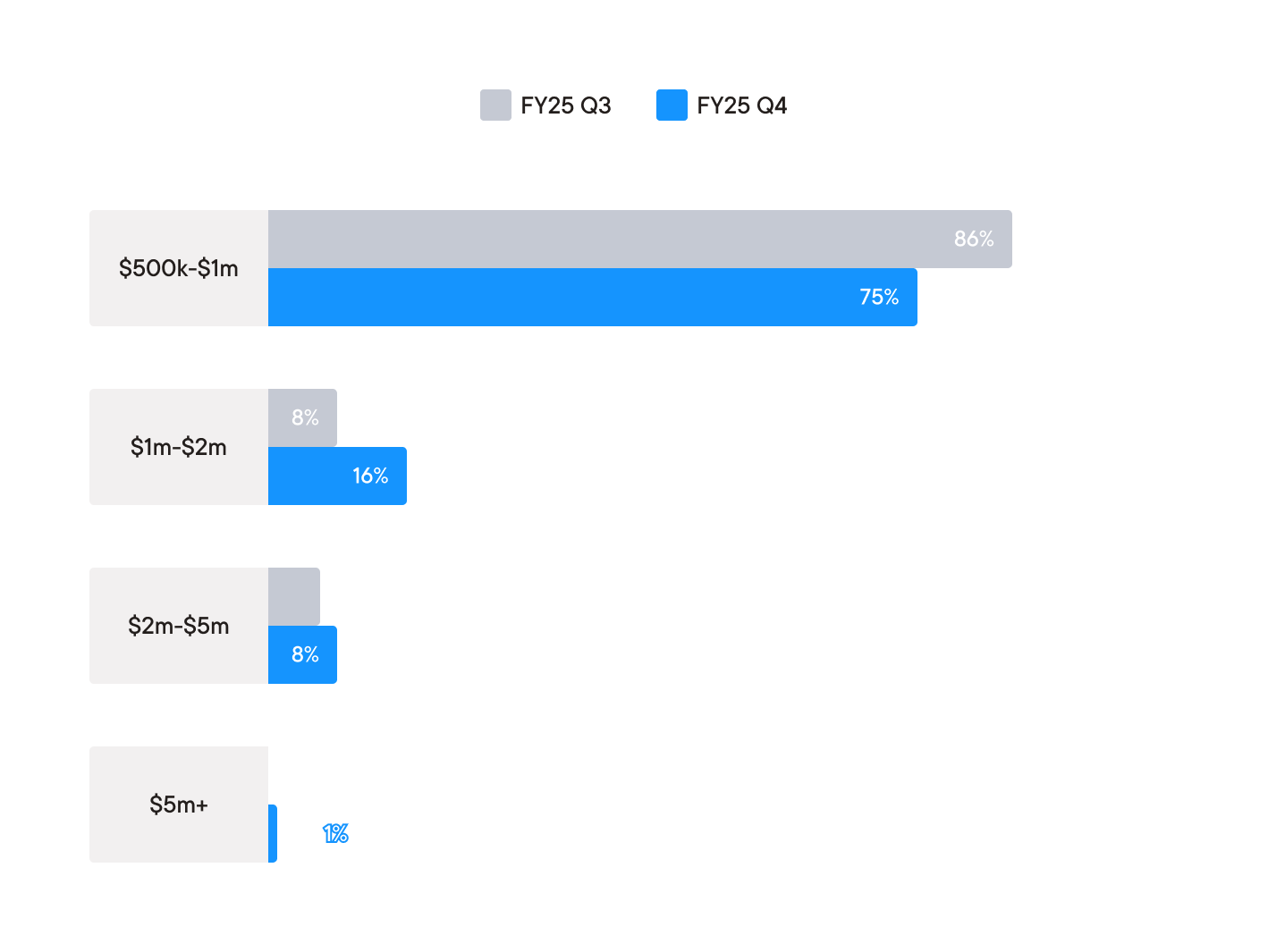

Sales by Price Range

In FY25 Q4, national sales data from channel agent partners reflected a widening distribution across higher price bands, influenced both by increased buyer appetite and stock availability on Development ID. While the $500k-$1m range remained the most prevalent, at 75%, this was down from 86% in FY25 Q3

In contrast, the $1m-$2m segment doubled to 16%, and $2m-$5m sales rose to 8%, pointing to stronger movement in mid-to-upper tiers of the market. Notably, $5m+ transactions appeared at 1%, suggesting some uplift in prestige stock activity and availability through the platform.

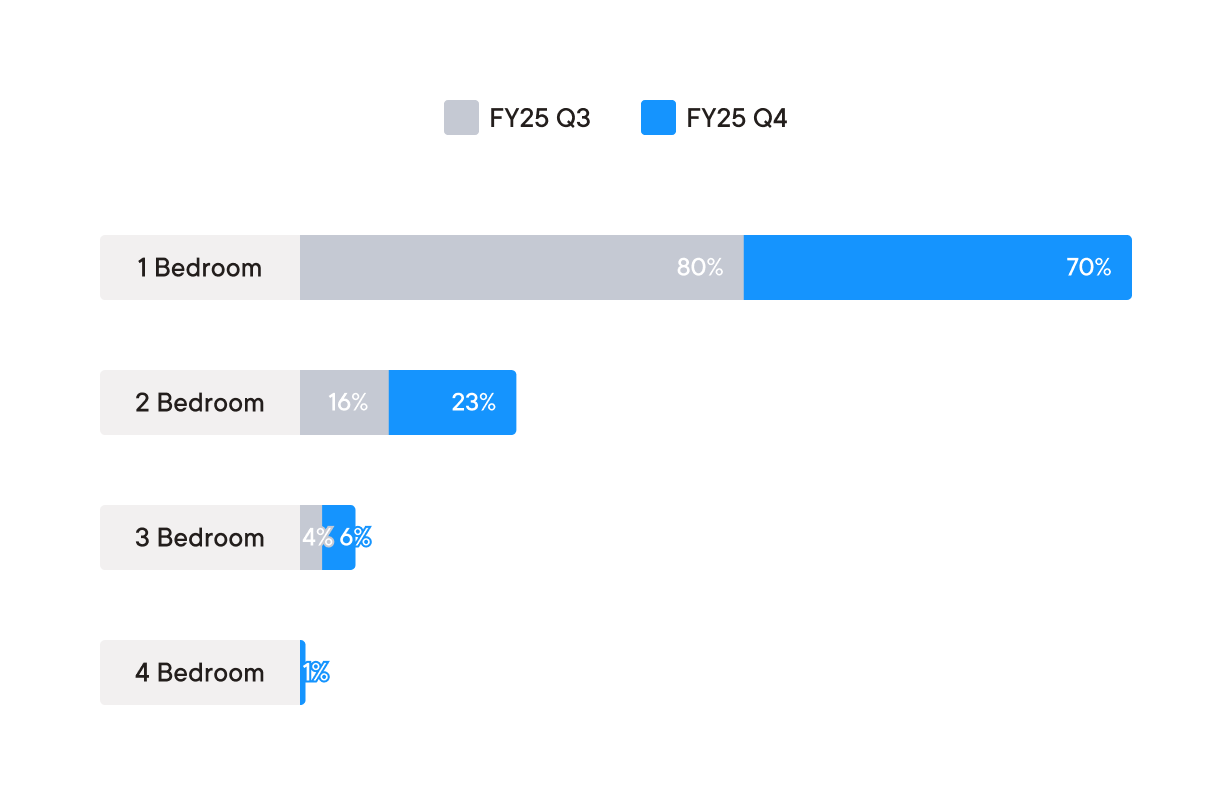

Sales by Bedroom

In FY25 Q4, the composition of transacted stock on Development ID shifted notably by bedroom count. 1-bedroom dwellings remained dominant at 70%, though down from 80% last quarter, indicating a modest diversification in product.

2-bedroom sales increased to 23% (up from 16%), suggesting rising demand for more spacious layouts or a shift in available stock. Larger formats also saw a lift, with 3-bedroom transactions rising to 6%, and 4-bedroom product accounting for 1%, reappearing this quarter after being absent in FY25 Q3.

To read the full report, click here.