We recently released our FY25 Q4 Off-the-Plan Market Insights Report which explores buyer intent and engagement in the off-the-plan residential estate market, leveraging comprehensive data from a-d.com.au.

Below takes a further dive into the national market buyer segment behaviour in FY25 Q4 compared to FY25 Q3.

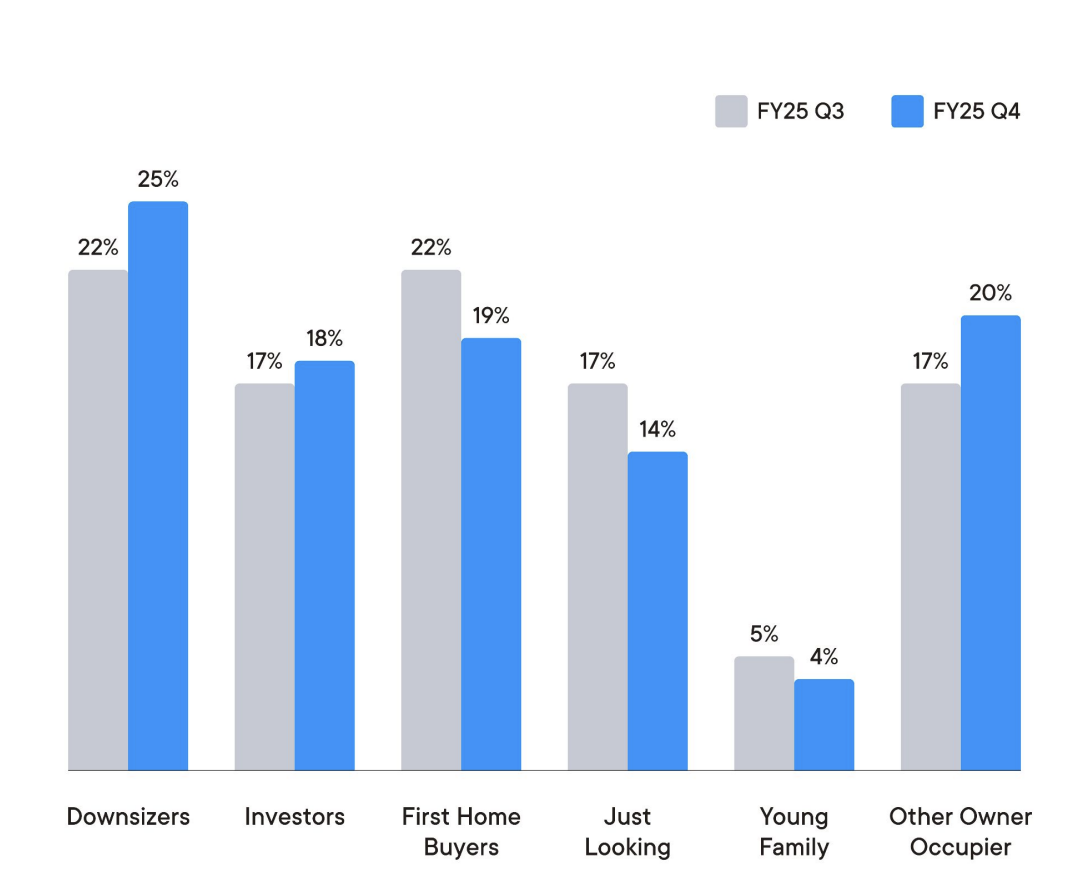

In FY25 Q4, national buyer types showed more defined shifts compared to last quarter, with Downsizers reclaiming the lead as the largest segment, rising from 22% to 25%. Other Owner Occupiers also saw a lift to 20%, recovering from their FY25 Q3 dip.

First Home Buyer activity softened slightly to 19%, following last quarter’s uplift, while Investor interest edged up again to 18%, continuing a cautious upward trend. The Just Looking market declined from 17% to 14%, suggesting a portion of previously passive browsers are either converting or exiting. Young Families dipped marginally to 4%, maintaining a small yet stable presence in the market.

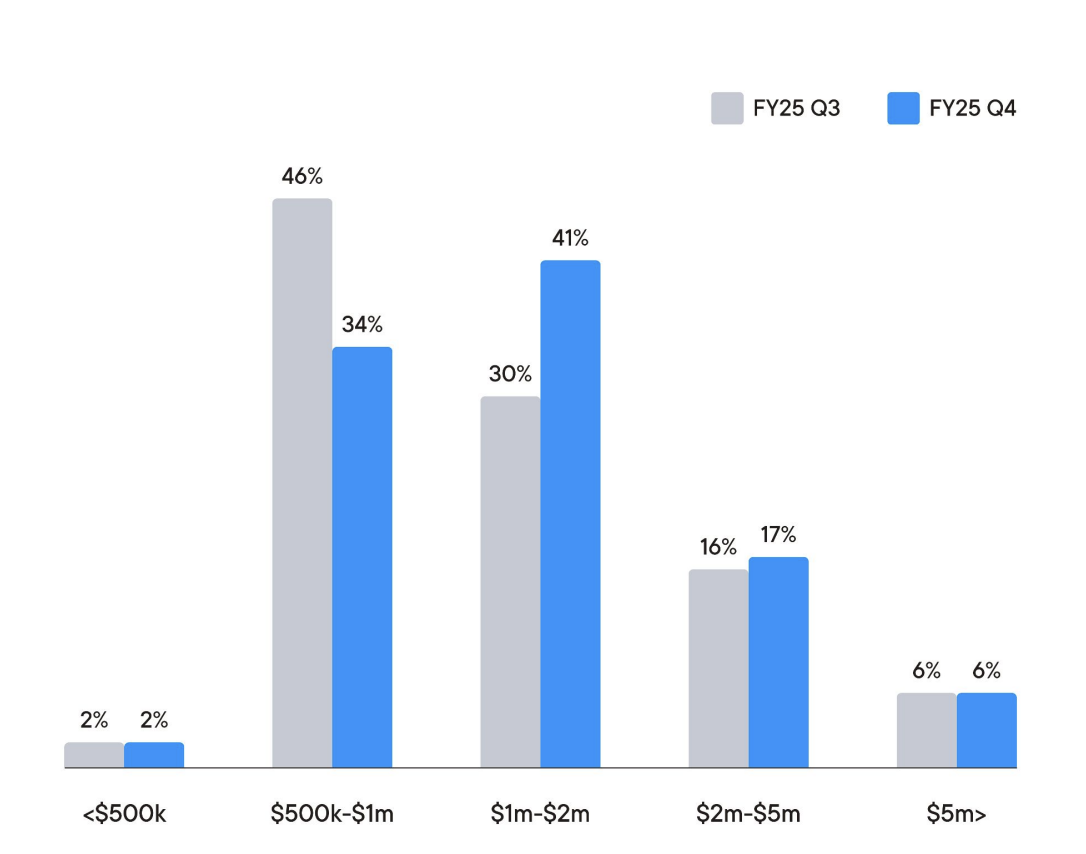

In FY25 Q4, there was a notable shift toward higher budget brackets nationally. The $1m-$2M range overtook $500k-$1m as the dominant price point, rising from 30% to 41%, while the mid-tier $500k-$1m budget range dropped back from 46%to 34%.

Budgets between $2m-$5m remained stable at 17%, and the prestige market ($5m+) held steady at 6%. Entry-level budgets under $500k continued to account for just 2% of buyer interest, reflecting both rising property prices and a limited supply of stock at this price point nationally.

In FY25 Q4, buyer timeframes - referring to how soon leads intend to make a purchase decision - remained largely stable, seeing only minor shifts. The 6-12 month window remained the most common at 25% (down from 26%), while the 3-6month and 1-3 month segments each edged up to 24% and 23% respectively.

Longer-term outlooks showed minimal change, with the 12-18 month group easing to 14% and the 18+ month segment holding steady, indicating a balanced mix of near-term and future purchase intent across the national market.

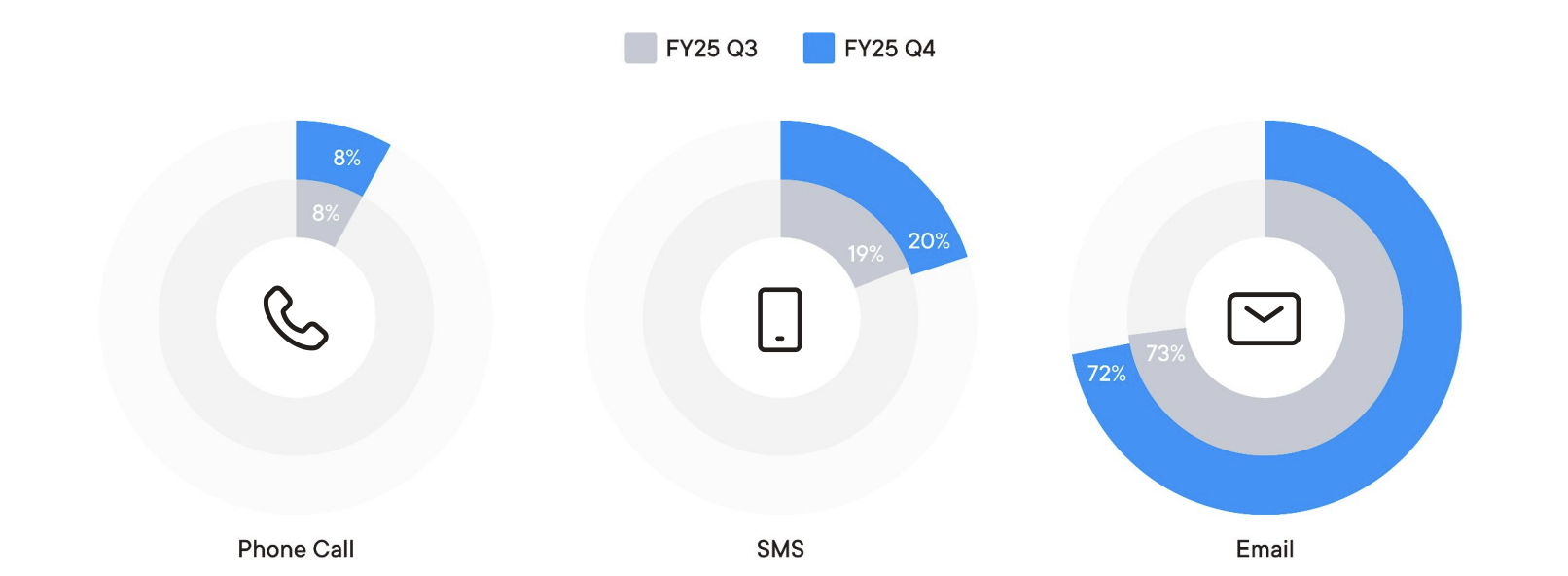

Preferred contact methods amongst leads remained consistent in FY25 Q4, with email continuing to dominate - coming in at 72%. SMS saw a slight rise to 20%, while phone contact held steady at 8%, reinforcing a clear preference for digital-first communication among project enquirers.

To read the full report, click here.